Wall Street is under stress on fading hopes of an early Fed pivot amid hawkish Fed talks & also Beige Book coupled with an escalating war of words between Israel and Iran after a war of friendly drones/missiles on the weekend. Gold was also moving in line with Iran-Israel saber rattling and Fed jawboning. Oil was also buoyed by Iran-Israel geopolitical tension despite the OPEC+ production cut narrative looking ineffective amid increasing production from the U.S., Canada and Brazil.

On early Friday Asian session, Gold spiked to almost 2418 from around 2375, while oil jumped to almost 86.50 from around 82.50 Dow Future plunged from around 38100 to almost 37500 and S&P 500 futures fell 60 points after news that Israel indeed launched the limited retaliation drone attack on harmless Iranian target (after duly informing US/Iran). This war drama follows a similar retaliation by Iran last Friday night, which looked like a badly scripted Hollywood war/spy thriller than any real war. In any way, by the early European session, Wall Street Futures recovered, while Gold also stumbled as Iran downplayed the ‘anonymous internal drone attack’ and does not want to escalate further by launching another Hollywood-style Drone thriller.

On early Asian morning Friday, Israel launched the much-awaited Iran retaliation to satisfy domestic political compulsion:

· Israel's response to Iranian attack may be imminent

· Israel's military chief of staff: There will be a response to Iran's launch of so many missiles and drones toward Israeli territory

· Israeli War Cabinet Vows Response to Iran as Oil Prices Cool Down

· Biden: The US is committed to Israeli security; The US is committed to protecting US interests and partners in the region, including Iraq

· US State Department: Hamas right now is the barrier and obstacle to a ceasefire in Gaza

· Israel had moved a "significant way" in submitting the proposal rejected by Hamas

· Iranian state media reports air defense systems were activated and three drones destroyed over the central city of Isfahan, as US media (ABC) quoted officials saying that Israel carried out an attack, supposedly Iran’s nuclear sites

· Tweets: IAEA can confirm that there is no damage to #Iran’s nuclear sites. DG @rafaelmgrossi continues to call for extreme restraint from everybody and reiterates that nuclear facilities should never be a target in military conflicts. IAEA is monitoring the situation very closely

· Iran’s news agency reported three explosions near an army base in the central city of Isfahan. An Iranian official said there was no missile attack and the explosions were the result of the activation of Iran’s air defense systems; Mini drones shot down by air defenses

· Senior Iranian official said no immediate plans for retaliation against Israel: “The foreign source of the incident has not been confirmed. We have not received any external attack, and the discussion leans more towards infiltration than attack”

· European Commission President Ursula von der Leyen calls on Iran, Israel and their allies to refrain from escalation in the Middle East: “It is necessary that the region remains stable and that all sides restrain from further action”

· China said it will continue to play a constructive role in de-escalating tensions in the Middle East: “China opposes any actions that further escalate tensions and will continue to play a constructive role to de-escalate the situation”

· Senior Israeli officials have declared a delay in the ground invasion of Rafah in Southern Gaza until an Israeli response against Iran has been concluded

· Yemen's Houthis Chief: There's no danger in maritime traffic related to ships linked to European countries that are not heading to Israel

· Iran's Foreign Minister tells a UN security council that Iran's defense and countermeasures have concluded and Israel must be compelled to stop any further military adventurism against our interests

· Iran's Foreign Minister says if any use of force by Israel or violation of Iran's sovereignty, Iran's response will be decisive and proper to make Israel regret its actions

· Iranian Foreign Minister: Iran had no other option but to attack Israel

· Iran's nuclear facilities are unharmed

· Iran says there have been no airstrikes, only shot-down quadcopter

· Israeli Missiles Strike Site in Iran - ABC News

· Senior Iranian Official: There is no plan for immediate retaliation; there is no clarification on who is behind the incident

On Thursday, global Ratings agency S&P cuts Israel’s long-term ratings to A-plus from AA-minus after the confrontation with Iran heightened last weekend and amid the already elevated geopolitical risks for Israel:

· We forecast that Israel’s general government deficit will widen to 8% of GDP in 2024, mostly as a result of increased defense spending

· Israel's long-term ratings lowered to 'A+' from 'AA-' due to increased geopolitical risk; negative outlook

· Israel's general government deficit to widen to 8% of GDP in 2024

· Israel's Higher Deficits to Remain, Net Government Debt to Peak at 66% of GDP in 2026

· Israel's Real Growth to be 0.5% in 2024

· Israeli finance ministry official attributes S&P long-term ratings cut to Iranian missile attack on Israel

On Thursday, Fed’s Bostic said:

· Inflation is too high and we still have a ways to go

· The pathway to 2% inflation will be slower than people expect, and bumpy

· Inflation is going where we want it to go, but it's slow

· I'm comfortable being patient

· I'm not in a mad dash hurry to get there

· I don't have a recession in my outlook

· We won't be able to reduce rates until towards the end of the year

· I think the economy will continue to grow as we get both mandates back in line

· We can keep rates steady as long as the labor market holds up

· The economy is slowing down but slowing down slowly

On Thursday, Fed’s Kashkari said:

· Housing resilience has been a surprise for me

· Once inflation is heading back to 2%, we can cut rates

· We need to be patient until convinced inflation falling

· We can wait as long as it takes before cutting rates

· Could potentially wait until 2025 to lower rates

On Thursday, Fed’s Mester said:

· More information is needed before confirming 2% inflation sustainability

· Inflation is slightly higher than anticipated this year

· Confidence is needed that inflation is decreasing

· Strong labor markets, solid economic growth

· Expects Inflation to Decrease

· Watching and Gathering More Information Before Taking Action

· Monetary Policy Well-Positioned

· Rates could stay put for longer if inflation doesn't reach 2%

· Possible rate cut if labor markets worsen

· Anticipates a Shift to Eased Policy

· States no rushed need to ease policy

· Inflation is higher than expected, need more confidence in the trajectory

On Thursday, Fed’s Bowman said:

· Inflation Progress Slows and Possibly Halts

· Ties strength of consumer spending to ongoing job growth

· Monetary policy is currently restrictive; time will tell if it is "sufficiently" restrictive

· Suggests consumers are turning to cheaper goods, but still spending heavily on travel for eclipse viewing

· Progress on inflation has slowed, perhaps stalled

· Emphasizes integrating AI into financial services for the Fed's understanding

· Emphasizes the need for guardrails on AI technology

On Thursday, Fed’s Williams said:

· The Fed is data-dependent, and the data have been very good

· Economic imbalances have been reduced

· I don't feel an urgency to cut rates

· Eventually, interest rates will need to be lower

· Rate cuts will be determined by economic activity

· If data called for higher rates, the Fed would hike

· Fed rate hikes are not my baseline forecast

· The economy is back on the pre-pandemic growth track

· I am watching the performance of China's economy

On Thursday, an economist Poll shows:

· The Federal Reserve is to first cut the Fed funds rate in September, say 54 of 100 economists

· Federal Reserve to cut rates by 50 basis points in 2024 say 50 of 100 economists; 34 say by more than 50 bps; four say no cuts

On Thursday, the G7 Finance Ministers summit statement said:

· Global economy resilient to multiple shocks, but growth prospects below historic averages

· Central Banks Committed to Achieving Price Stability

· Geo-political risks from Russia's war against Ukraine and the situation in the Middle East could impact trade, supply chains, and commodity prices

· Welcomes EU proposal to direct frozen Russian asset revenues to aid Ukraine

· Frozen Russian assets to be used to support Ukraine in all possible avenues

· Financial Stability and Regulatory Issues Vital to Protect Global Economy Against Threats

· Commitment to retain frozen Russian assets

· Concern over Crisis in Gaza

· Close coordination is guaranteed for future measures to reduce Iran's weapons acquisition, production, or transfer

· Calls for regional stability, notes economic risks of escalation in the area

· New Zealand joins Russian oil price cap coalition

· G7 urges multilateral development banks to collaborate in examining options for incorporating callable capital value into balance sheets

On Thursday, IMF's Managing Director Georgieva said:

· The US Fed is “doing the right thing’ on rates

· We shouldn't gear up for the rapid decline in rates

· I'm still optimistic the Fed will be able to cut rates in 2024

On Thursday, Netflix's Q1CY24 Earnings summary was upbeat:

· EPS $5.28, est. $4.52

· Revenue $9.378, est. $9.26b

· Streaming paid memberships 269.6m, est. 264.52m

· Streaming paid net change +9.33m, est. +4.84m

· APAC streaming paid net change +2.16m, est. +1.48m

· Sees 2Q EPS $4.68, est. $4.54

· Sees 2Q Revenue $9.49b, est. $9.51b

· Sees FY operating margin 25%, saw 24%, est. 24.1%

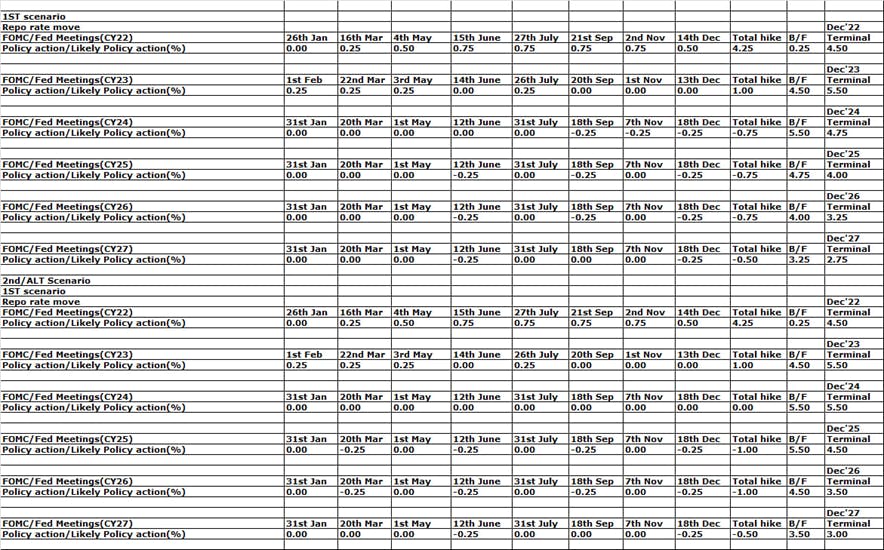

Overall the Fed is now preparing the market for rate cuts from Sep’24 or even no rate cuts in 2024; the Fed should not go for an early rate cut, while the economy is firing on almost all cylinders. Fed should hold for now and go for rate cuts when disinflation gets more momentum and there are some signs of labor market stress. For the time being, the Fed could continue to do the QT to bring B/S size down to around $6.60T and be ready for the next round of QE/QQE/Rate cuts. Fed may go for an early rate cut if the US labor market worsens unexpectedly or the rate of disinflation accelerates suddenly.

The 6M rolling average of US core inflation (PCE+CPI) is now around +3.5%. Fed may cut 75 bps in H2CY24 if the 6M rolling average of core inflation (PCE+CPI) indeed eased further to +3.0% by H1CY24. The Fed wants to keep the real/neutral rate around +1.0% in the longer term (assuming +3.0% repo rate and +2.0% core inflation). But in the meantime, till core inflation/headline inflation goes down to around 2.00% on a sustainable basis, the Fed wants to maintain the real rate at around present restrictive levels of +1.50% (assuming the present repo rate +5.50% and 2023 average core CPI around +4.00%).

As per Taylor’s rule, for the US:

Recommended policy repo rate (I) = A+B+(C-D)*(E-B)

=1.50+2.00+ (2.60-2.00)*(4.50.00-2.00) =1.00+2+ (0.60*2.50) = 3.00+1.50=4.50% (By Dec’24)

Here:

A=desired real interest rate=1.50; B= inflation target =2.00; C= Actual real GDP growth rate for CY23=2.6; D= Real GDP growth rate target/potential=2.00; E= average core CPI+PCE inflation for CY23=4.50

The Fed may go for -75 bps rate cuts in September, November, and December’24. By 18th September (Fed MPC date), the Fed will have complete data for core inflation and also unemployment/real GDP data for H1CY24 and also Aug/July’24 to have the required ‘higher confidence’ to go for rate cuts. Fed may bring down the repo rate to +4.75% by Dec’24 from present +5.50%.

Fed may announce a plan for QT tapering/trajectory/closing in the May meeting and should have closed the same before going for any rate cuts cycle. Fed, the world’s most important central bank may not continue QT (even at a reduced pace) and go for rate cuts at the same time as QT, and rate cuts are contradictory (like QE and rate hikes). But Fed/Powell kept that absurd option of simultaneous QT and rate cuts open, at least theoretically. Thus assuming a bizarre phenomenon, the Fed may go for -75 bps rate cuts in H2CY24, most probably from Sep’24 after deciding about the possible B/S size to ensure money market stability

Looking ahead, the Fed may keep B/S size around $6.60T, around pre-COVID levels to ensure financial/Wall Street stability along with Main Street stability (price stability and employment stability). Fed’s B/S size is presently (Mar’24 end) around $7.48T around 25% of estimated nominal GDP for $30T by Dec’24. Depending upon the actual rate/reaction in the repo/funding market, the Fed may taper the QT from the present $0.095T/M to 0.050-0.075T/M for 18-12 months from May’24;i.e. Fed may end the QT by May’25-Dec’25 at B/S size around $6.60T. This is lower than the earlier market estimate of $7.00T and thus should be seen as more hawkish. Also, rate cuts along with QT (even with slower pace/tapering) should be less hawkish.

Ahead of the Nov’23 U.S. Presidential election, White House/Biden/Fed/Powell is more concerned about elevated inflation rather than the labor market; prices of essential goods & services are still significantly higher (around +20%) than pre-COVID levels, which is creating some anti-incumbency wave (dissatisfaction) among general voters against Biden admin (Democrats) on some economic issues (higher cost of living).

Thus Fed is now giving more priority to price stability than employment (which is still hovering below the 4% red line) and is not ready to cut rates early as it may again cause higher inflation just ahead of the November election. Fed may hike only from Septenber’24, which will ensure no inflation spike just ahead of the Nov’24 election (as any rate action usually takes 6-12 months to transmit in the real economy), while boosting up both Wall Street and also Main Street (investors/traders/voters). Fed hiked rate last on 26th July’23 and may continue to be on hold till at least July’24; i.e. around 12 months for full/proper transmission of its +5.25% cumulative rate hikes effect into the real economy.

Overall, the Fed’s mandate is to ensure price stability (2% core inflation), and maximum employment (below 4% unemployment rate) along with financial/Wall Street stability as well as lower borrowing costs for the government. As the US is now paying almost 15% of its tax revenue as interest on debt, the Fed will now not allow the 10Y US bond yield above 4.50-5.00% at any cost (against present levels of average core CPI around +4.0%).

But the Fed may also blink on rate cuts in H2CY24 just before the US election:

Ahead of Nov’24 US Presidential election, as evident in the last Congressional testimony, the Fed is under huge pressure from opposition Republican lawmakers (Trump) and also supporters for ‘assisting’ Biden admin (Democrats) in booting the election win probability by facilitating rate cuts. Thus Fed may not go for any rate cuts till Nov’24 or even Dec’24 to show that it’s politically independent. In the meantime, the Fed may close the QT at the present pace of around -0.095T/M for the next nine months (April-Dec’24) for the targeted ample B/S size around $6.60T (@22% of CY24 nominal GDP around $30T, just above 20% minimum requirement of $6.00T).

The most logical step would be Fed to close the QT completely before going for a rate cuts cycle and then go for any QE, if required to counter another economic crisis down the years. Fed has to prepare its B/S for the next round of QQE and thus has to normalize the B/S first.

Now going by various Fed comments in the last few weeks, it seems the Fed is ‘extremely’ worried about the pace of slower disinflation. Fed is also apparently confused about the dual combination of QT, even at a slower pace (QT taper) and rate cuts in the months ahead as these two instruments (tools) are contradictory/opposite (like if Fed goes for QE and rate hikes at the same time). Ideally, the Fed should finish the QT first for a proper B/S size (bank reserve) to ensure ample liquidity for the US funding/money/REPO market.

But the Fed may continue QT (even at a slower pace) and go for a rate cut cycle at the same time despite these two policy actions being contradictory. Thus the Fed may go for rate cuts of -75 bps cumulatively in September, November, and December’24 for +4.75% repo rates from the present +5.50%. Fed may bring down further its B/S size from present around $7.5T to $6.55T through QT tapering by May-Dec’25 to keep minimum/ample liquidity for the US funding/money market and also to prepare itself for the next cycle of QE, whatever may be the next recession excuse.

The market is now expecting 3-2 rate cuts (75-50 bps) in 2024, while some Fed policymakers are now arguing for lesser rate cuts of 1-2 rate cuts or even no rate cuts at all. Looking ahead, the Fed may not cut rates at all in 2024 considering the slower rate of disinflation, political issues ahead of the Nov’24 election, and the logic that it should not go for any rate cuts while doing QT, which is the opposite. Also, the reduction of B/S from around $8.97T to around $6.60T (projected); i.e. around $2.50T (~$2.37T) reduction over 2.5-3.00 years is equivalent to a rate hike of around +50 bps (higher 2Y bond yield).

In that scenario, if the US core CPI average for 2024 comes down to around +3.00% by Dec’24 from present levels of +3.8%, the Fed may cut rates by -100 bps in 2025 for a repo rate +4.50% (from present +5.50%) for a real restrictive repo rate +1.50% (repo rate 4.50%-3.00% projected average core cpi for 2024). Presently, the real restrictive repo rate is also around +1.50% (repo rate 5.50%-4.00% average core CPI for 2023).

At present, in its last (Mar’24) SEP/dot-plots, the Fed projected -75 bps rate cuts each in 2024, 2025, and 2026 and -50 bps rate cuts in 2027 for a terminal neutral repo rate +2.75% against pre-COVID neutral repo rate +2.50%. Now various Fed policymakers are arguing for a slightly higher neutral repo rate at +3.00% against projected core CPI of +2.00%; i.e. neutral real rate at +1.00%.

Thus depending upon the actual trajectory of core CPI, the Fed may cut -100 bps each in 2025, 2026, and -50 bps in 2027 for a terminal neutral repo rate of +3.00% from the present +5.50%. Fed had boosted its B/S from around $3.86T in late September’2019 (after the QT tantrum) to around $8.97T in Apr’22; i.e. over $5T in a matter of 32 months (@0.16T/M) to fight previous QT and COVID induced financial crisis.

Now Fed may announce a plan for QT tapering from $0.095T/M to $0.075/M and end the QT by 15th Mar’25 around B/S size $6.60T before going for any rate cuts from mid-March’25; Fed may opt for four QTR rate cuts (-25 bps) each in each quarter in 2025, 2026 and two half yearly rate cuts in 2027 to ensure price/employment/financial stability. Although, the Fed’s official QT rate is -$0.095T/M ($90B/M), in reality, the effective average QT rate is already around -$0.073T/M. As the Fed is now managing the funding/money market through ON/RRP, there is a lower risk of a 2019 type of QT tantrum this time.

Fed’s mandate is now 2% price stability (core inflation), below 4% unemployment rate, and below 4.75-5.00% US 10Y bond yield to ensure lower borrowing costs for the government and overall financial stability. Fed, as well as ECB, BOE, and BOC, are now struggling to keep bond yield and inflation at their preferred range despite non-stop jawboning; perhaps they are talking too much too early and thus FX market is not being influenced by them significantly, moving in a narrow range. The BOJ is now trying to talk down the USDJPY desperately, presently hovering around 152 levels, causing higher imported inflation and a higher cost of living back home, although it may be beneficial for exports. However, most of the Japanese are not happy at all due to higher imported inflation in Japan for the devalued currency.

Bottom line:

Original scenario: -75 bps rate cuts each in 2024, 2025, 2026, and -50 bps in 2027 for a neutral repo rate of +2.75%

If the rate of disinflation accelerates, the Fed may go for -75 bps rate cuts each in 2024, 2025, and 2026 and -50 bps in 2027. Fed may continue the QT (even at an officially slower pace) and rate cuts at the same time (in 2024) despite being contradictory.

Alternate scenario: -100 bps rate cuts each in 2025, 2026, and -50 bps in 2027 for terminal neutral reo rate +3.00%

Fed may announce a plan for QT tapering from -$0.095T/M to -$0.075T/M from April’24 (even before the May’24 meeting) and close the QT by Mar’25 at B/S around $6.60T. Then Fed may start the rate cut cycle from Mar’25 with -100 bps rate cuts each in 2025, 2026 (@-25 bps at each QTR), and finally -50 bps in 2027 (@-25 bps in Q2 and Q4).

Market impact:

On Thursday, Wall Street Futures edged down on fading hopes of an early Fed pivot, and an escalating war of words (scripted) between Iran and Israel in line with their respective domestic political compulsions; Gold was getting some support on geopolitical tensions.

Wall Street was also undercut by hawkish Fed talks as Powell & Co is now preparing the market for no rate cuts in 2024, although there is also a probability of rate cuts from Sep’24. Fed Chair Powell and also VC Jefferson clearly said that the disinflation progress stalled, while the labor market and overall economy were still running hot. Thus Fed has to keep higher for a longer policy (restrictive) at least till H1CY24 or even till Q1CY25.

On Thursday, Wall Street was boosted by commination services, utilities, consumer staples, banks & financials, materials, real estate, and healthcare to some extent, while dragged by techs, consumer discretionary, industrials, and energy. Wall Street was also boosted by United Health, Travelers, Nike, Verizon, P&G Chevron, and JPM, while dragged by Microsoft, Intel, Salesforce, Amazon and IBM.

Technical trading levels: DJ-30, NQ-100 Future, and Gold

Whatever may be the narrative, technically Dow Future (38000), now has to sustain over 38100 for a further rally to 38400/38675 and 38800/39050-39200/40000-40200/40425-40600/40700 to 42600 levels in the coming days; otherwise, sustaining below 38050-37650-37500, may further fall to 37400/37200-37050/36600 and 36300/36300 and even 35700 levels in the coming days.

Similarly, NQ-100 Future (17500) now has to sustain over 17800-18000 for a rebound to 18500-18750 and 19000/19200-19450/19775 and 20000/20200 in the coming days; otherwise, sustaining below 17750, NQ-100 may again fall to around 17800/17575*-17150/16850 and 16650/16490-15900/15700 in the coming days.

Also, technically Gold (XAU/USD: 2383) now has to sustain over 2400-2425 for any further rally to 2455-2475/2500; otherwise sustaining below 2395-2390, may again fall to 2375/2350 and 2320/2315-2305/2300 and 2290/2270-22245/2240, and 2220/2210-2200/2195-2190/2180 and 2175/2145*, and further to 2120/2110-2100/2080-2060/2039 and 2020/2010-2000-1995/1985-1975 and even 1940 may be on the card.

The materials contained on this document are not made by iFOREX but by an independent third party and should not in any way be construed, either explicitly or implicitly, directly or indirectly, as investment advice, recommendation or suggestion of an investment strategy with respect to a financial instrument, in any manner whatsoever. Any indication of past performance or simulated past performance included in this document is not a reliable indicator of future results. For the full disclaimer click here.

Join iFOREX to get an education package and start taking advantage of market opportunities.

A beginner's e-book

A beginner's e-book $5,000 practice demo account

$5,000 practice demo account A 12-part video course

A 12-part video course